For the past few months, tax season had all of us looking backward at 2025 returns, at what the new law changed, at what already happened. That part’s done.

So for the next little while, a few of us are going to do the opposite. We’re starting a series, one tax strategy per post, looking forward at the moves still on the table before this year closes. Most of the best planning happens before December, not after. By April, the window is usually shut.

We’ll start with the strategy we bring up more than any other: the Roth conversion.

What it actually is

A Roth conversion means moving money out of a traditional IRA and into a Roth IRA, and voluntarily paying the tax on it now.

That’s the whole idea: pay some tax today so you don’t pay (likely more) tax later. Money in a traditional IRA has never been taxed; every dollar that comes out in retirement will be. Money in a Roth has already been taxed, so it grows and comes out tax-free for you, and eventually for whoever inherits it.

When it tends to make sense

A conversion isn’t right for everyone, every year. But there are windows where it’s worth a hard look.

The years after you retire but before required minimum distributions begin, income is often lower in that stretch, which means a conversion can be done at a lower tax rate.

A year your income dips for any reason. Lower income, lower rate, cheaper conversion.

A year the market is down. If your IRA balance has fallen, you can convert the same shares for less tax, and the recovery happens inside the Roth, tax-free.

And if you believe tax rates are headed up over your lifetime, converting locks in today’s rate.

The part people get wrong

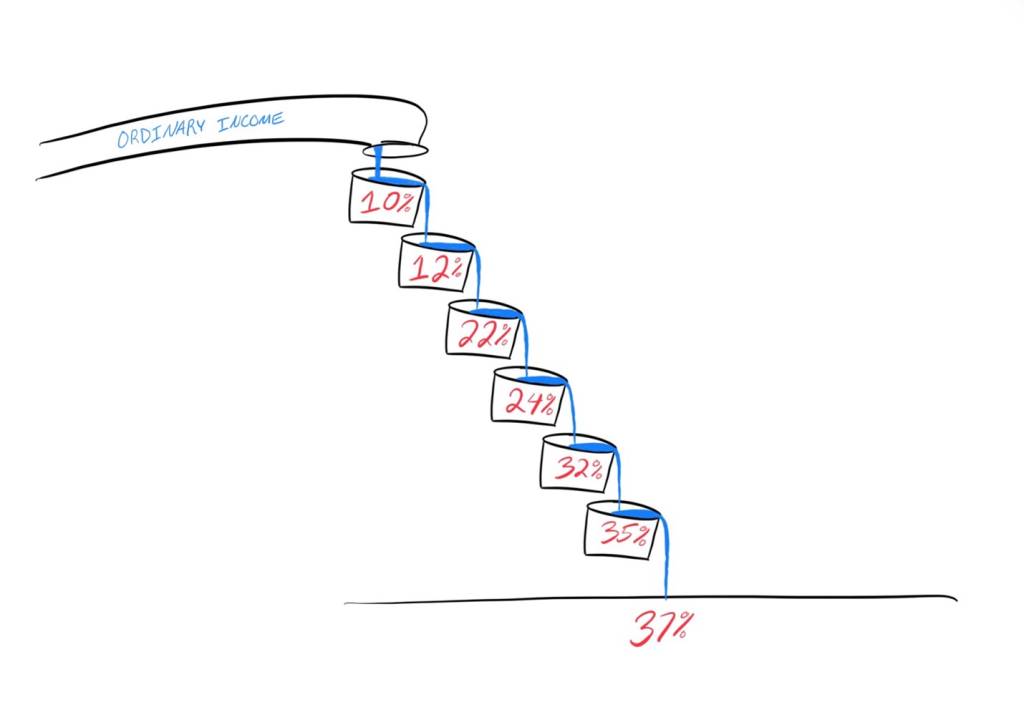

The goal is not to convert as much as possible. The goal is to convert the right amount.

A conversion adds to your taxable income for the year. Convert too much and you can push yourself into a higher bracket, or trip an income threshold that raises your Medicare premiums two years later. (That Medicare piece is its own conversation, and it’s coming later in this series.)

Done well, a conversion fills up the room you have in your current bracket and stops there. That’s the difference between a conversion that helps and one that just shuffles the tax bill around.

Why it’s worth the trouble

A well-sized conversion does a few things at once. It gives you a pool of money in retirement you can draw on without adding to your tax bill. It removes those dollars from future required distributions. And it hands your children or grandchildren an asset they can inherit tax-free.

None of that happens by accident. It happens because someone ran the numbers in the right year, for the right amount.

If you’d like to know whether a conversion makes sense for you, and how much, that’s exactly the kind of thing we’d map out together. Here’s how to start a conversation with us.

Bain Nickels, CFP®, CKA®

Disclosure: Traditional IRA account owners have considerations to make before performing a Roth IRA conversion. These primarily include income tax consequences on the converted amount in the year of conversion, withdrawal limitations from a Roth IRA, and income limitations for future contributions to a Roth IRA. In addition, if you are required to take a required minimum distribution (RMD) in the year you convert, you must do so before converting to a Roth IRA. (22-LPL)